Robust and Bayesian Regression Comparison

Robust techniques and variable selection can help us obtain more stable linear fits. In this post, I used return regressions against returns on State Street sctors ETFs to test this fact. By computing out-of-sample regression, I contrast the performance of OLS regression, robust regression(huber and tukey) and positive lasso regressions.

|

|

1. Import EOD from Quandl

First we load ETF and stocks that satisfies our requirements. By requirement we are saying each of the following stocks

- Has 41 days of adj close prices from 2019/01/01 to 2019/03/01 inclusive, and

- Can give 1, 3 and 6 non-zero betas from Lasso (both with and without positive beta restriction) regression for later analysis.

The full list of tickers are as below:

|

|

Now we start actual loading.

|

|

Compute each ticker’s daily return and then seperate the return into in-sample (the first 20 days) and out-of-sample (the last 20 days) data.

|

|

2. Regression

In this part we perform regressions one by one. For each regression, we first run in-sample fitting to get the optimal configs (if any) and the in-sample betas. Then using the in-sample optimal configs we run out-of-sample regression to get the same amount of coefficients to calculate the in-to-out beta L2 norm as our robustness metric.

A. OLS regression

First is OLS regression.

a. In-sample

No optimization is required in OLS.

|

|

b. Out-of-sample

As there’s no optimization, we simply rerun the same regression against the out-of-sample dataset.

|

|

c. L2 norm

The L2 norm is calculated and stored for later analysis.

|

|

AADR 1.353710

AAON 5.330675

ACER 4.029213

ACIW 4.501306

ACLS 6.978846

ACM 1.882538

ACT 1.235258

ACWF 0.918673

ACWI 0.740807

ACWX 1.695779

ADT 5.984692

AFT 1.338696

AFTY 4.282447

AGD 2.287036

AGO_P_B 1.096079

AHT 8.060704

AIEQ 0.888335

AIG_WS 14.980616

AIRR 1.498807

ALKS 4.509373

ALL 2.427588

ALXN 4.066937

AMGN 3.331021

AMN 13.501120

AMNB 3.191322

AMOT 2.786852

ANDE 3.685212

ANSS 3.813627

AOA 0.673246

AON 3.456226

dtype: float64

B. Huber

In Huber regression we have a penalty term with parameter t. Therefore we have the ability to optimize this t for in-sample fitting.

a. In-sample

We use grid search to perform the optimization.

|

|

b. Out-of-sample

We use the optimal t we found to run out-of-sample regression.

|

|

c. L2 norm

|

|

AADR 1.390011

AAON 5.330675

ACER 4.029213

ACIW 4.520645

ACLS 6.978846

ACM 1.723419

ACT 1.177438

ACWF 0.914225

ACWI 0.740807

ACWX 1.716467

ADT 5.984692

AFT 1.338696

AFTY 3.177647

AGD 2.287036

AGO_P_B 0.926278

AHT 8.060704

AIEQ 0.847107

AIG_WS 14.980616

AIRR 1.498807

ALKS 5.871315

ALL 2.642671

ALXN 4.030956

AMGN 3.331021

AMN 13.499555

AMNB 3.274254

AMOT 2.786852

ANDE 3.685212

ANSS 3.833712

AOA 0.742647

AON 3.454299

dtype: float64

C. Tukey

In Tukey regression there is, similar to Huber reg, a parameter c which is integers.

a. In-sample

We run grid search on c to find its optima based on minimizing in-sample MSE of residuals.

|

|

b. Out-of-sample

Using in-sample optimal c we run out-of-sample regression to get the other half set of betas.

|

|

c. L2 norm

|

|

AADR 1.354184

AAON 5.331992

ACER 4.027493

ACIW 4.502004

ACLS 6.981216

ACM 1.880968

ACT 1.234964

ACWF 0.918660

ACWI 0.740829

ACWX 1.695937

ADT 5.980670

AFT 1.339173

AFTY 4.280923

AGD 2.286033

AGO_P_B 1.095972

AHT 8.060488

AIEQ 0.887859

AIG_WS 14.974489

AIRR 1.499437

ALKS 4.503220

ALL 2.428550

ALXN 4.066387

AMGN 3.326690

AMN 13.498992

AMNB 3.191148

AMOT 2.787551

ANDE 3.686052

ANSS 3.813933

AOA 0.674376

AON 3.455658

dtype: float64

D. Lasso

In regular Lasso regression, we adjust the penalty parameter $\alpha$ to tune the number of non-zero betas. Same as above, we optimize w.r.t. to $\alpha$ to find in-sample optimality but this time we use $R^2$.

a. In-sample

We run grid search on $\alpha$ to find optimal parameters for all different target numbers of non-zero betas (in this problem: 1, 3 or 6).

|

|

b. Out-of-sample

For each different n, we run out-of-sample regression with corresponding in-sample optimal $\alpha$.

|

|

c. L2 norm

|

|

n = 1

AADR 0.155828

AAON 0.175003

ACER 0.872036

ACIW 0.620643

ACLS 0.744314

ACM 0.314417

ACT 0.034371

ACWF 0.344031

ACWI 0.322220

ACWX 0.290820

ADT 0.100632

AFT 0.121234

AFTY 0.075920

AGD 0.126845

AGO_P_B 0.072990

AHT 0.640832

AIEQ 0.312616

AIG_WS 1.016887

AIRR 0.103753

ALKS 0.536951

ALL 0.251199

ALXN 0.006286

AMGN 0.210962

AMN 1.172191

AMNB 0.000303

AMOT 0.003382

ANDE 0.089362

ANSS 0.707883

AOA 0.238605

AON 0.215213

dtype: float64

n = 3

AADR 0.317361

AAON 0.646347

ACER 1.097086

ACIW 0.852599

ACLS 0.970315

ACM 0.311965

ACT 0.190420

ACWF 0.333636

ACWI 0.349658

ACWX 0.367570

ADT 0.413495

AFT 0.170364

AFTY 0.369955

AGD 0.392622

AGO_P_B 0.194950

AHT 0.628096

AIEQ 0.430564

AIG_WS 0.898526

AIRR 0.353337

ALKS 0.627170

ALL 0.551264

ALXN 0.458300

AMGN 0.292862

AMN 2.806067

AMNB 0.145884

AMOT 0.734125

ANDE 0.293687

ANSS 0.735479

AOA 0.254537

AON 1.214032

dtype: float64

n = 6

AADR 0.456563

AAON 0.955433

ACER 1.462182

ACIW 1.853961

ACLS 1.720626

ACM 0.866007

ACT 0.597189

ACWF 0.418556

ACWI 0.215605

ACWX 0.563101

ADT 1.361210

AFT 0.438779

AFTY 1.736157

AGD 0.391316

AGO_P_B 0.377466

AHT 6.894572

AIEQ 0.320238

AIG_WS 5.080266

AIRR 0.694890

ALKS 1.043629

ALL 1.120698

ALXN 1.023300

AMGN 0.724205

AMN 5.609016

AMNB 1.287305

AMOT 2.139451

ANDE 1.551472

ANSS 0.552735

AOA 0.269326

AON 2.595071

dtype: float64

E. Positive Lasso

Same as regular Lasso except this time not only do we restrict on the number of non-zero betas, but also we want the remaining betas to be positive.

a. In-sample

|

|

b. Out-of-sample

|

|

c. L2 norm

|

|

n = 1

AADR 0.155828

AAON 0.175003

ACER 0.872036

ACIW 0.620643

ACLS 0.744314

ACM 0.314417

ACT 0.034371

ACWF 0.344031

ACWI 0.322220

ACWX 0.290820

ADT 0.100632

AFT 0.121234

AFTY 0.075920

AGD 0.126845

AGO_P_B 0.072990

AHT 0.640832

AIEQ 0.312616

AIG_WS 1.016887

AIRR 0.103753

ALKS 0.536951

ALL 0.236938

ALXN 0.006286

AMGN 0.210962

AMN 0.263691

AMNB 0.000303

AMOT 0.003382

ANDE 0.089362

ANSS 0.707883

AOA 0.238605

AON 0.215213

dtype: float64

n = 3

AADR 0.317361

AAON 0.646347

ACER 1.097086

ACIW 0.984273

ACLS 1.057114

ACM 0.311965

ACT 0.190420

ACWF 0.333636

ACWI 0.349658

ACWX 0.367570

ADT 0.413495

AFT 0.170364

AFTY 0.369955

AGD 0.392622

AGO_P_B 0.194871

AHT 0.628096

AIEQ 0.430564

AIG_WS 0.898526

AIRR 0.353337

ALKS 0.627170

ALL 0.232596

ALXN 0.458300

AMGN 0.292862

AMN 0.311460

AMNB 0.145884

AMOT 0.919254

ANDE 1.715678

ANSS 0.735479

AOA 0.254537

AON 0.636419

dtype: float64

n = 6

AADR 0.456563

AAON 1.125961

ACER 3.032427

ACIW 2.936279

ACLS 2.805377

ACM 0.704292

ACT 0.668765

ACWF 0.418557

ACWI 0.215605

ACWX 0.455908

ADT 3.932955

AFT 0.696588

AFTY 0.310241

AGD 1.169620

AGO_P_B 0.300354

AHT 1.592437

AIEQ 0.320238

AIG_WS 1.443177

AIRR 0.798543

ALKS 2.875320

ALL 0.670975

ALXN 1.770219

AMGN 1.618411

AMN 1.340530

AMNB 0.592686

AMOT 1.332605

ANDE 0.530865

ANSS 1.356940

AOA 0.269326

AON 1.066722

dtype: float64

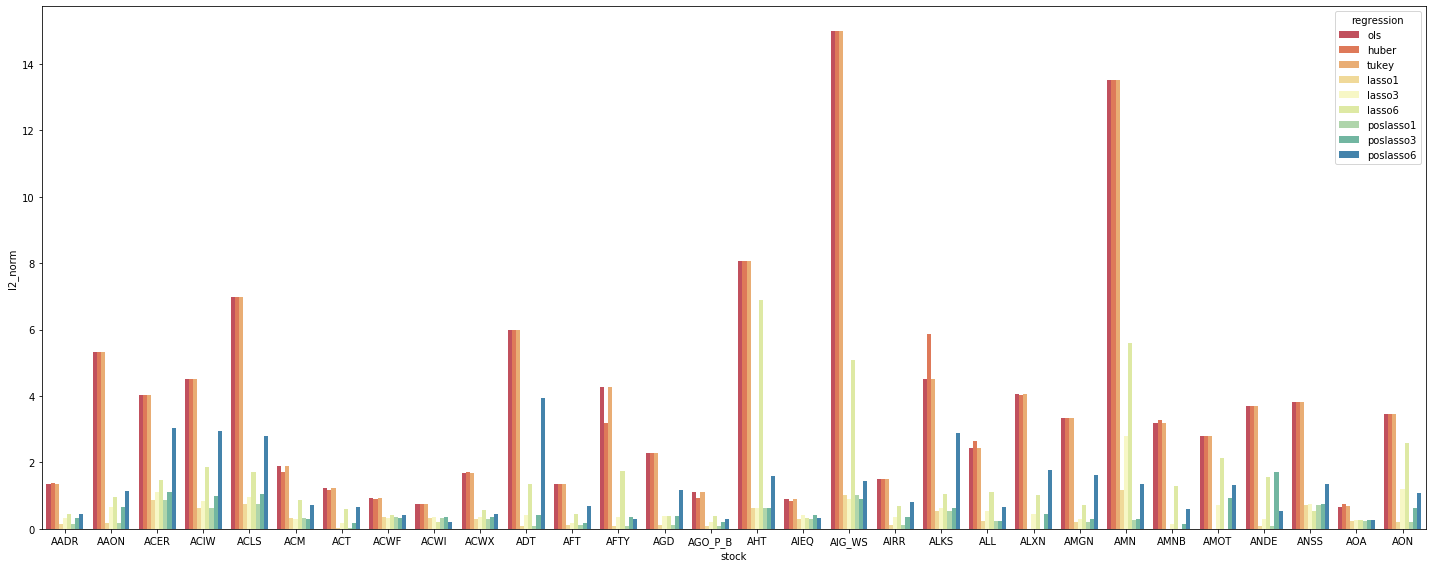

3. Comparison

Now that all in-to-out L2 norms of betas are calculated, we can start on comparison between these regressions.

L2 Table

A summarized large table would be

|

|

| stock | ols | huber | tukey | lasso1 | lasso3 | lasso6 | poslasso1 | poslasso3 | poslasso6 |

|---|---|---|---|---|---|---|---|---|---|

| AADR | 1.353710 | 1.390011 | 1.354184 | 0.155828 | 0.317361 | 0.456563 | 0.155828 | 0.317361 | 0.456563 |

| AAON | 5.330675 | 5.330675 | 5.331992 | 0.175003 | 0.646347 | 0.955433 | 0.175003 | 0.646347 | 1.125961 |

| ACER | 4.029213 | 4.029213 | 4.027493 | 0.872036 | 1.097086 | 1.462182 | 0.872036 | 1.097086 | 3.032427 |

| ACIW | 4.501306 | 4.520645 | 4.502004 | 0.620643 | 0.852599 | 1.853961 | 0.620643 | 0.984273 | 2.936279 |

| ACLS | 6.978846 | 6.978846 | 6.981216 | 0.744314 | 0.970315 | 1.720626 | 0.744314 | 1.057114 | 2.805377 |

| ACM | 1.882538 | 1.723419 | 1.880968 | 0.314417 | 0.311965 | 0.866007 | 0.314417 | 0.311965 | 0.704292 |

| ACT | 1.235258 | 1.177438 | 1.234964 | 0.034371 | 0.190420 | 0.597189 | 0.034371 | 0.190420 | 0.668765 |

| ACWF | 0.918673 | 0.914225 | 0.918660 | 0.344031 | 0.333636 | 0.418556 | 0.344031 | 0.333636 | 0.418557 |

| ACWI | 0.740807 | 0.740807 | 0.740829 | 0.322220 | 0.349658 | 0.215605 | 0.322220 | 0.349658 | 0.215605 |

| ACWX | 1.695779 | 1.716467 | 1.695937 | 0.290820 | 0.367570 | 0.563101 | 0.290820 | 0.367570 | 0.455908 |

| ADT | 5.984692 | 5.984692 | 5.980670 | 0.100632 | 0.413495 | 1.361210 | 0.100632 | 0.413495 | 3.932955 |

| AFT | 1.338696 | 1.338696 | 1.339173 | 0.121234 | 0.170364 | 0.438779 | 0.121234 | 0.170364 | 0.696588 |

| AFTY | 4.282447 | 3.177647 | 4.280923 | 0.075920 | 0.369955 | 1.736157 | 0.075920 | 0.369955 | 0.310241 |

| AGD | 2.287036 | 2.287036 | 2.286033 | 0.126845 | 0.392622 | 0.391316 | 0.126845 | 0.392622 | 1.169620 |

| AGO_P_B | 1.096079 | 0.926278 | 1.095972 | 0.072990 | 0.194950 | 0.377466 | 0.072990 | 0.194871 | 0.300354 |

| AHT | 8.060704 | 8.060704 | 8.060488 | 0.640832 | 0.628096 | 6.894572 | 0.640832 | 0.628096 | 1.592437 |

| AIEQ | 0.888335 | 0.847107 | 0.887859 | 0.312616 | 0.430564 | 0.320238 | 0.312616 | 0.430564 | 0.320238 |

| AIG_WS | 14.980616 | 14.980616 | 14.974489 | 1.016887 | 0.898526 | 5.080266 | 1.016887 | 0.898526 | 1.443177 |

| AIRR | 1.498807 | 1.498807 | 1.499437 | 0.103753 | 0.353337 | 0.694890 | 0.103753 | 0.353337 | 0.798543 |

| ALKS | 4.509373 | 5.871315 | 4.503220 | 0.536951 | 0.627170 | 1.043629 | 0.536951 | 0.627170 | 2.875320 |

| ALL | 2.427588 | 2.642671 | 2.428550 | 0.251199 | 0.551264 | 1.120698 | 0.236938 | 0.232596 | 0.670975 |

| ALXN | 4.066937 | 4.030956 | 4.066387 | 0.006286 | 0.458300 | 1.023300 | 0.006286 | 0.458300 | 1.770219 |

| AMGN | 3.331021 | 3.331021 | 3.326690 | 0.210962 | 0.292862 | 0.724205 | 0.210962 | 0.292862 | 1.618411 |

| AMN | 13.501120 | 13.499555 | 13.498992 | 1.172191 | 2.806067 | 5.609016 | 0.263691 | 0.311460 | 1.340530 |

| AMNB | 3.191322 | 3.274254 | 3.191148 | 0.000303 | 0.145884 | 1.287305 | 0.000303 | 0.145884 | 0.592686 |

| AMOT | 2.786852 | 2.786852 | 2.787551 | 0.003382 | 0.734125 | 2.139451 | 0.003382 | 0.919254 | 1.332605 |

| ANDE | 3.685212 | 3.685212 | 3.686052 | 0.089362 | 0.293687 | 1.551472 | 0.089362 | 1.715678 | 0.530865 |

| ANSS | 3.813627 | 3.833712 | 3.813933 | 0.707883 | 0.735479 | 0.552735 | 0.707883 | 0.735479 | 1.356940 |

| AOA | 0.673246 | 0.742647 | 0.674376 | 0.238605 | 0.254537 | 0.269326 | 0.238605 | 0.254537 | 0.269326 |

| AON | 3.456226 | 3.454299 | 3.455658 | 0.215213 | 1.214032 | 2.595071 | 0.215213 | 0.636419 | 1.066722 |

Histogram

We can do a lot of things with this table, first of which would be plotting all data points on a summary histogram.

|

|

According to the grouped histogram above, in many cases positive Lasso with 1 or 3 non-zero betas are most robust amongst all regression types. More generally, we observe (in robustness) the following order

- Positive Lasso with 1 or 3 non-zero betas

- Regular Lasso with 1 or 3 non-zero betas

- Regular Lasso with 6 non-zero betas

- Positive Lasso with 6 non-zero betas

- Tukey, Huber and OLS are giving visually same robustness

The last three regression come really similar which is out of our expectation. In contrast, the improvement of Lasso is significant, both without and with restriction of positive betas. We are seeing some improvement of over 90% decreases in L2 norm of beta differences from in-sample to out-of-sample regression, which directly describes the robustness of the underlying regression.

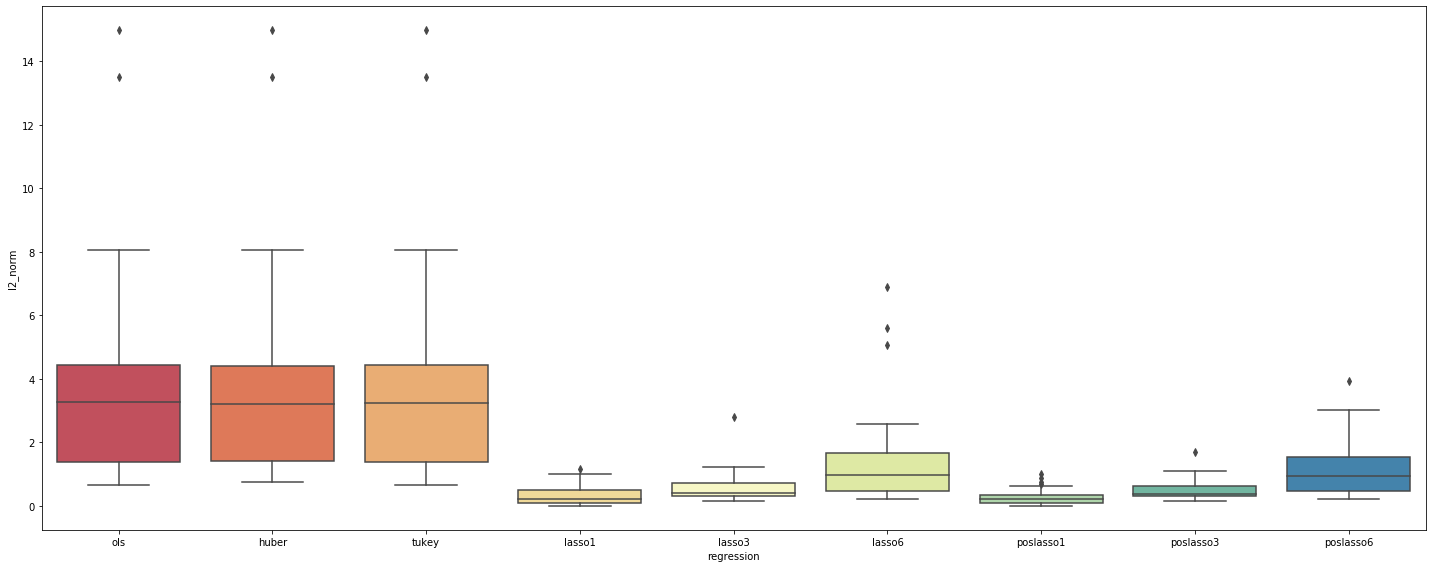

Box Plot

In addition to the histogram, we may also drop the individual stocks’ info and go one step further, by taking a look at the box plots.

|

|

Box plot above gives a statistically speaking more summarized view on the overall robustness of the regressions. Now that we’ve excluded the idiosyncratic differences in this plot, the regressions robustness order becomes more clear:

- Lasso (both with and without positive beta restriction) with 1 or 3 non-zero betas

- Lasso (both with and without positive beta restriction) with 6 non-zero betas

- OLS, Tukey and Huber

where the last three are the least robust, both from the dispersion of the L2 norm values and from the greater means (and outliers).

Talking about outliers, we do notice there’re some non-trivial advantage of having fewer non-zero betas: Lasso (both with and without positive beta restriction) with 1 non-zero beta is better than 3 and then 6 in that its outliers are visually smaller and closer to distribution means. While lasso6 and poslasso6 above are giving “extremer” extremes, the outliers given by lasso1 and poslasso1 are just trivial enough for us to make this conclusion.

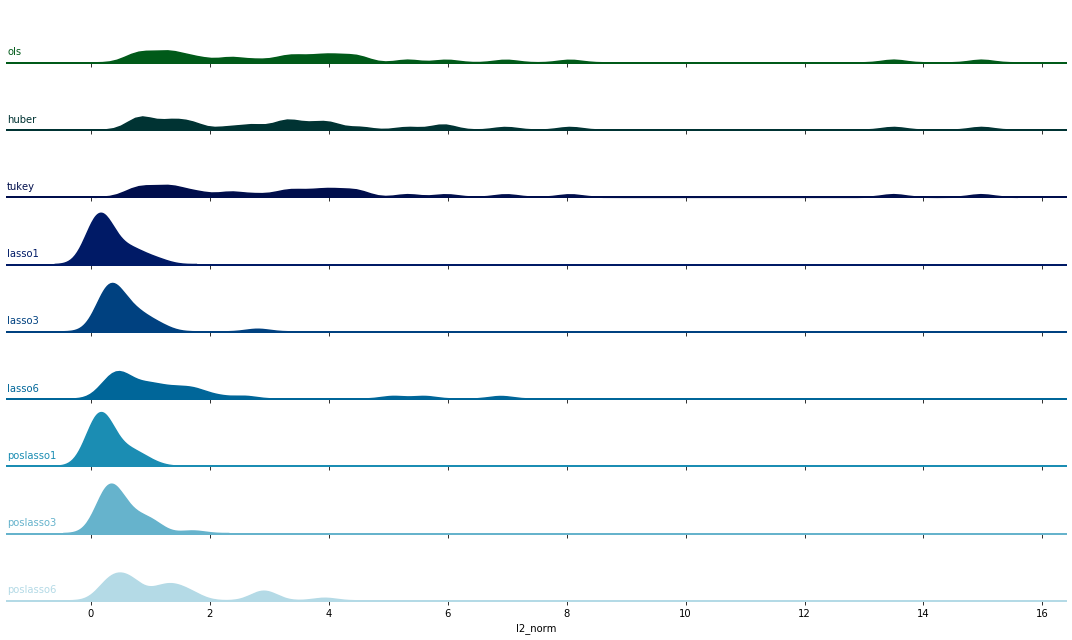

Dist Plot

Another observation comes from the skewness of the above distributions. One may easily notice that all distributions are skewed toward the same direction: positive. We may get it verified by running skewness tests but rather let us just plot them here.

|

|

The dist plot above coincides with our observation: the right tail is much longer and fatter than left.