Comparison Between Exponential Weighted and Rolling Regression

This research discusses two normal prediction ways people are using: exponential weighted regression and rolling regression. By comparing the prediction errors of both ways, we generally get the idea of the difference between these two regressions.

1. Introduction

Comparison between two ways of regression

- Exponential Weighted Moving Regression: considering all the previous data to do the regression, however, following the intuition that the nearer data have more effects on the future data, the weight of data are different regarding time. Time decay applies here.

- Rolling Regression: for each date, we determine a moving boxcar window so that our prediction is based on a certain range of past data. The disadvantage of this method is that it could not smoothly decay old data and sometimes when an outlier is added or discarded, the prediction will change a lot.

Benchmark

We set the out-of-sample regression coefficient here as our benchmark to see which way of regression could give us a better prediction (lower prediction errors).

Another thing worth mentioning is that we’re using SPY(S&P 500 ETF Trust) to do the regression and prediction.

2. Data Preparation

Introduction of the packages in the research

We’re using several really important python pac

- Pandas: dataframe manipulation

- NumPy: support for mathematical functions and computation of arrays and matrics

- Quandl: source of our financial data

- Statsmodel: statistical analysis

- Matplotlib: plot tools

- tqdm: progress bar

- os: interact with the operating system

- PandasRollingOLS: package for computing rolling regression and obtain the coefficients

|

|

|

|

Obtaining data

Get the list of tickers that Quandl has and filter the tickers that could satisfy our conditions: tickers which have valid records from 2016-01-04 to 2019-12-31.

|

|

0 A

1 AA

2 AAAU

3 AACG

4 AADR

...

8627 ZUO

8628 ZVO

8629 ZYME

8630 ZYNE

8631 ZYXI

Name: Ticker, Length: 8632, dtype: object

For the tickers we selected, compute the daily return using daily Adjusted Closing Price.

|

|

Also, add SPY into the EOD list.

|

|

Current number of tickers: 201

3. Computation of regressions

Exponential weighted regression

For the exponential weighted regression, we set $\frac{1}{\lambda}$ to be the characteristic time of our averaging, so $\alpha = 1 - e^{-\lambda \delta t}$ is the smoothing factor. Since our data is daily, $\delta t$ = 1.

By using the relationship between those variables, we set two functions in order to calculate our $\alpha$ and window given $\lambda$.

|

|

Just for example, we choose $\lambda$ = 0.01.

|

|

(0.01, 0.009950166250831893, 200)

Compute exponential-weighted coefficient.

|

|

In-Sample Rolling Regression

Given the lambda we have, window size = 200 here.

|

|

Out-of-sample regression

|

|

[Timestamp('2018-07-27 00:00:00'),

Timestamp('2019-01-28 00:00:00'),

Timestamp('2019-07-26 00:00:00'),

Timestamp('2019-12-27 00:00:00')]

|

|

4. Statistical Comparison

To compare the performance of the above two regressions, I used several ways.

Comparison of MAE and MSE of the prediction

- MAE: MAE measures the average magnitude of the errors in a set of predictions

- MSE: MSE measures the average magnitude of the error

For both indexes, the smaller, the more accurate the prediction is.

|

|

|

|

For exponential-weighted regression, the prediction's MAE=0.5353, MSE=1.1382;

For rolling regression, the prediction's MAE=0.5587, MSE=1.1956

From the result, we could see that the exponential-wegithed regression’s MAE and MSE are both smaller than that of rolling regression, which means the in this case, the exponential weighted regression is preferred.

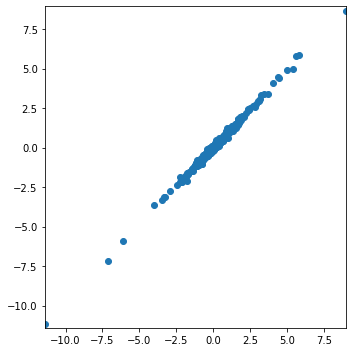

Relationship between beta(from exponential regression) and b(from rolling regression)

Drawing the scatter plot of the two regressions’ prediction erros of all the tickers by the two different regression, I tried to see if there’s any relationships between those two predictions’ errors.

|

|

| c | beta | b | |

|---|---|---|---|

| 0 | 1.314779 | 1.236790 | 1.174681 |

| 1 | 0.830983 | 1.002387 | 1.058264 |

| 2 | 1.371328 | 1.229957 | 1.121128 |

| 3 | 1.062639 | 1.307811 | 1.474886 |

| 4 | 0.797373 | 0.820776 | 0.855415 |

| … | … | … | … |

| 799 | 0.817802 | 0.079735 | 0.152021 |

| 800 | 0.429854 | 0.794702 | 0.769725 |

| 801 | 0.923952 | 0.941771 | 0.951230 |

| 802 | 1.141867 | 1.062994 | 1.024160 |

| 803 | 1.384714 | 1.116091 | 1.170909 |

|

|

| abs_err_beta | abs_err_b | err_beta | err_b | |

|---|---|---|---|---|

| 0 | 0.077989 | 0.140098 | 0.077989 | 0.140098 |

| 1 | 0.171404 | 0.227281 | -0.171404 | -0.227281 |

| 2 | 0.141371 | 0.250201 | 0.141371 | 0.250201 |

| 3 | 0.245172 | 0.412247 | -0.245172 | -0.412247 |

| 4 | 0.023403 | 0.058042 | -0.023403 | -0.058042 |

| … | … | … | … | … |

| 799 | 0.738067 | 0.665781 | 0.738067 | 0.665781 |

| 800 | 0.364849 | 0.339871 | -0.364849 | -0.339871 |

| 801 | 0.017819 | 0.027278 | -0.017819 | -0.027278 |

| 802 | 0.078873 | 0.117707 | 0.078873 | 0.117707 |

| 803 | 0.268623 | 0.213806 | 0.268623 | 0.213806 |

|

|

By checking the scatter plot, we could see that they’re forming a almost linear relationship. Because of this, we run a regression between those two coefficients’ prediction errors to see the coefficient of the regression.

|

|

OLS Regression Results

=======================================================================================

Dep. Variable: err_beta R-squared (uncentered): 0.994

Model: OLS Adj. R-squared (uncentered): 0.994

Method: Least Squares F-statistic: 1.386e+05

Date: Thu, 14 May 2020 Prob (F-statistic): 0.00

Time: 16:30:22 Log-Likelihood: 880.22

No. Observations: 804 AIC: -1758.

Df Residuals: 803 BIC: -1754.

Df Model: 1

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

err_b 0.9729 0.003 372.315 0.000 0.968 0.978

==============================================================================

Omnibus: 83.087 Durbin-Watson: 2.752

Prob(Omnibus): 0.000 Jarque-Bera (JB): 354.569

Skew: 0.376 Prob(JB): 1.01e-77

Kurtosis: 6.165 Cond. No. 1.00

==============================================================================

Warnings:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

From the result, we could see that the cofficient of the regression is almost 1, which means the prediction error of the two regressions are very close. However, since it’s still not 1, we could get the relationship that Error_exponential = 0.9729 * Error_rolling. So, the exponential regression is more accurate here.

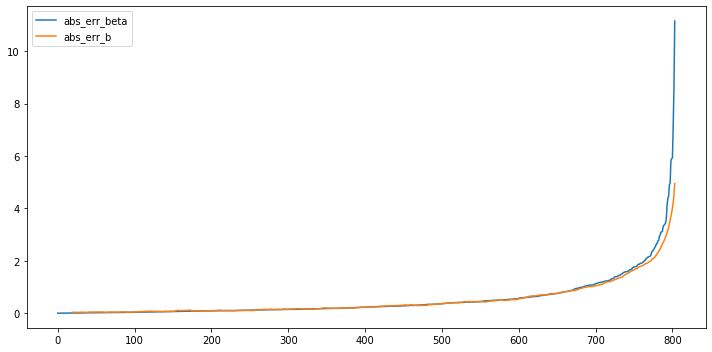

Plot of the absolute error of two regressions.

By sorting the absolute value of exponential regression model and then plot the prediction errors of those two regressions, we could tell that the result are pretty close. The only obvious difference is when absolute error of exponential weighted regression is extremely high, the absolute error of rolling regression is lower.

|

|

5. Play with more $\lambda s$

Using only one lambda is pretty limited here. So we dig into the exploration and try different lambda (different windows) here to see if there’re any patterns behind it.

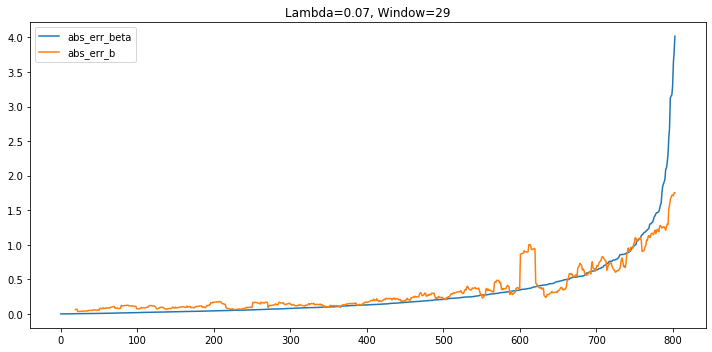

Following, I chose $\lambda$ = 0.07, 0.05, 0.03 and 0.009. The corresponding window for the rolling regression here is: 29, 47, 60, 222.

In order to make the computation easier, I rewrote the above code and make it a function which takes $\lambda$ as input.

|

|

$\lambda$ = 0.07, window = 29

|

|

For exponential-weighted regression, the prediction's MAE=0.3028, MSE=0.3219;

For rolling regression, the prediction's MAE=0.3434, MSE=0.4840

OLS Regression Results

==============================================================================

Dep. Variable: err_beta R-squared: 0.372

Model: OLS Adj. R-squared: 0.371

Method: Least Squares F-statistic: 475.0

Date: Thu, 14 May 2020 Prob (F-statistic): 4.50e-83

Time: 19:08:53 Log-Likelihood: -498.01

No. Observations: 804 AIC: 1000.

Df Residuals: 802 BIC: 1009.

Df Model: 1

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

Intercept 0.0012 0.016 0.076 0.939 -0.030 0.032

err_b 0.4976 0.023 21.795 0.000 0.453 0.542

==============================================================================

Omnibus: 484.829 Durbin-Watson: 2.069

Prob(Omnibus): 0.000 Jarque-Bera (JB): 25718.642

Skew: 1.999 Prob(JB): 0.00

Kurtosis: 30.418 Cond. No. 1.44

==============================================================================

Warnings:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

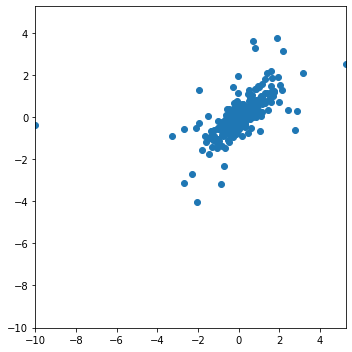

From the scatter plot and also the regression summary, we could see that the prediction errors of the two regressions are less linear correlated. After plotting the prediction errors, from the plot, we could see that for most of the time, the absolute error of rolling regression is higher and the exponential weighted regression’s prediction is more accurate (as the MAE and MSE shows).

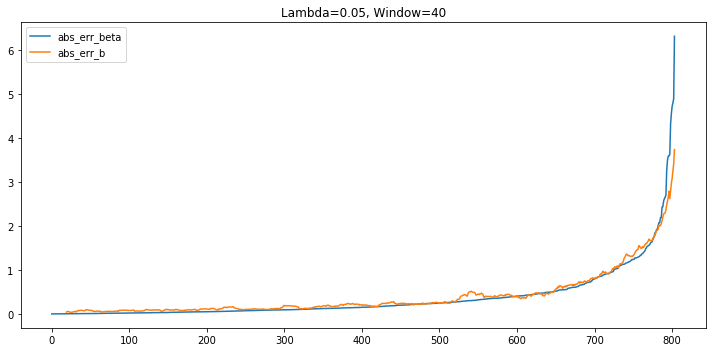

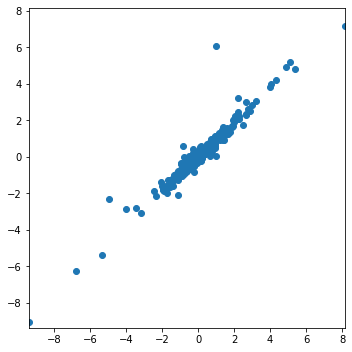

$\lambda$ = 0.05, window = 40

|

|

For exponential-weighted regression, the prediction's MAE=0.3741, MSE=0.5525;

For rolling regression, the prediction's MAE=0.4540, MSE=0.7896

OLS Regression Results

==============================================================================

Dep. Variable: err_beta R-squared: 0.878

Model: OLS Adj. R-squared: 0.878

Method: Least Squares F-statistic: 5796.

Date: Thu, 14 May 2020 Prob (F-statistic): 0.00

Time: 17:26:21 Log-Likelihood: -54.356

No. Observations: 804 AIC: 112.7

Df Residuals: 802 BIC: 122.1

Df Model: 1

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

Intercept -0.0062 0.009 -0.678 0.498 -0.024 0.012

err_b 0.7845 0.010 76.131 0.000 0.764 0.805

==============================================================================

Omnibus: 828.136 Durbin-Watson: 1.963

Prob(Omnibus): 0.000 Jarque-Bera (JB): 245095.795

Skew: 4.105 Prob(JB): 0.00

Kurtosis: 88.140 Cond. No. 1.14

==============================================================================

Warnings:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

Things are very similar with the previous one. Here, for most of the time, the prediction error of rolling regression is higher than that of exponential regression. However, the difference between the two mothods are shrinking.

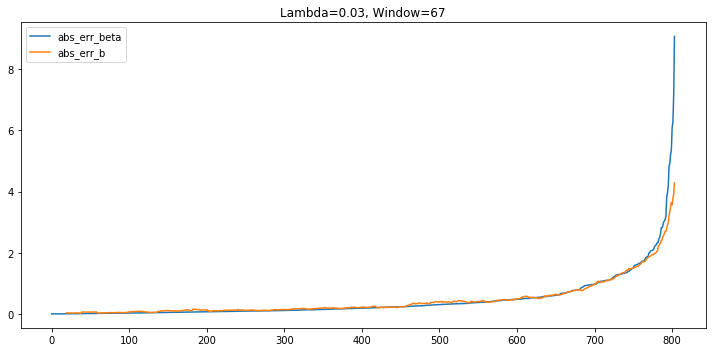

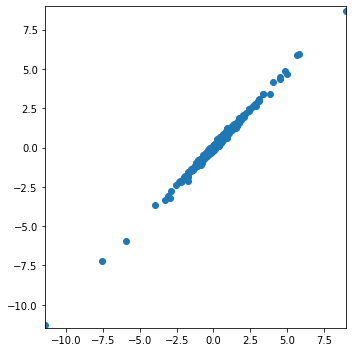

$\lambda$ = 0.03, window = 67

|

|

For exponential-weighted regression, the prediction's MAE=0.4600, MSE=0.8762;

For rolling regression, the prediction's MAE=0.5081, MSE=0.9748

OLS Regression Results

==============================================================================

Dep. Variable: err_beta R-squared: 0.925

Model: OLS Adj. R-squared: 0.925

Method: Least Squares F-statistic: 9962.

Date: Thu, 14 May 2020 Prob (F-statistic): 0.00

Time: 17:27:46 Log-Likelihood: -42.657

No. Observations: 804 AIC: 89.31

Df Residuals: 802 BIC: 98.69

Df Model: 1

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

Intercept 0.0124 0.009 1.372 0.171 -0.005 0.030

err_b 0.9116 0.009 99.809 0.000 0.894 0.930

==============================================================================

Omnibus: 1403.599 Durbin-Watson: 2.011

Prob(Omnibus): 0.000 Jarque-Bera (JB): 1510276.440

Skew: 11.096 Prob(JB): 0.00

Kurtosis: 214.164 Cond. No. 1.04

==============================================================================

Warnings:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

As the window is widening, rolling regression is improving. However, exponential weighted regression is still preferred here.

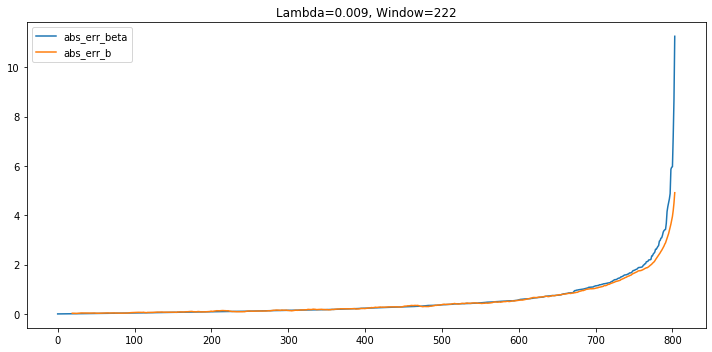

$\lambda$ = 0.009, window = 222

|

|

For exponential-weighted regression, the prediction's MAE=0.5388, MSE=1.1476;

For rolling regression, the prediction's MAE=0.5571, MSE=1.1940

OLS Regression Results

==============================================================================

Dep. Variable: err_beta R-squared: 0.995

Model: OLS Adj. R-squared: 0.995

Method: Least Squares F-statistic: 1.503e+05

Date: Thu, 14 May 2020 Prob (F-statistic): 0.00

Time: 17:25:35 Log-Likelihood: 910.91

No. Observations: 804 AIC: -1818.

Df Residuals: 802 BIC: -1808.

Df Model: 1

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

Intercept 0.0007 0.003 0.241 0.810 -0.005 0.006

err_b 0.9777 0.003 387.675 0.000 0.973 0.983

==============================================================================

Omnibus: 85.769 Durbin-Watson: 2.566

Prob(Omnibus): 0.000 Jarque-Bera (JB): 580.498

Skew: -0.152 Prob(JB): 8.84e-127

Kurtosis: 7.152 Cond. No. 1.11

==============================================================================

Warnings:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

Most of the time, the performance of the two regressions are very close. Except for the extreme case when the error of exponential weighted regression is high, then the rolling regression is more preferred.

6. Conclusion

From the performances we get above, we could conclude that overall, the performance of exponential weighted regression is better and the prediction is more accurate. The limitation of the rolling regression is that comparing with exponential weighted regression, the information it gets is not enough. So, as the $\lambda$ gets smaller, which implies the window of the rolling regression is larger, the performance is better and closer to exponential weighted regression, which suggests us that in order to improve the rolling regression, we should widen the window.

However, we could not just widen our window unlimitedly. The edge of rolling regression is that its more reactive and responsive to the real-time market change. When something huge happens, it will immediately reflect on the regression and the prediction. When the window of rolling regression is larger, the effect of real-time information will be smaller, which is not good for activities such as high-frequency trading.